The real estate sector occupies a unique and often uneasy position within the GST framework. Unlike most industries, it operates at the intersection of land (outside GST), construction (taxable as service), long-term projects, staggered consideration flows, and complex development structures.

While the 2019 rate restructuring appeared to stabilise the regime, litigation has by no means subsided. Disputes today revolve less around rates and more around input tax credit restrictions, valuation in joint development models, treatment of ancillary recoveries, and the continuing shadow of anti-profiteering proceedings.

This article examines the current legal position in depth, with reference to statutory provisions, notifications, and key judicial precedents.

I. The Foundational Principle – When Does GST Apply in Real Estate?

Under Schedule III of the CGST Act, 2017, sale of land and sale of building after issuance of completion certificate (or first occupation) are neither supply of goods nor supply of services.

When a developer constructs a complex, building, civil structure or any part thereof for sale to a buyer before obtaining the completion certificate, the law treats it as a supply of service under Schedule II. Courts had already examined and settled this distinction even under the pre-GST regime.

In Larsen & Toubro Ltd. v. State of Karnataka (2013) 65 VST 1 (SC), the Supreme Court held that a developer entering into agreements with purchasers prior to completion undertakes a works contract liable to tax on the construction component.

GST substantially adopts this principle.

Thus:

-

Completed property → Outside GST

-

Under-construction property → Taxable as construction service

The real complexity begins after this foundational classification.

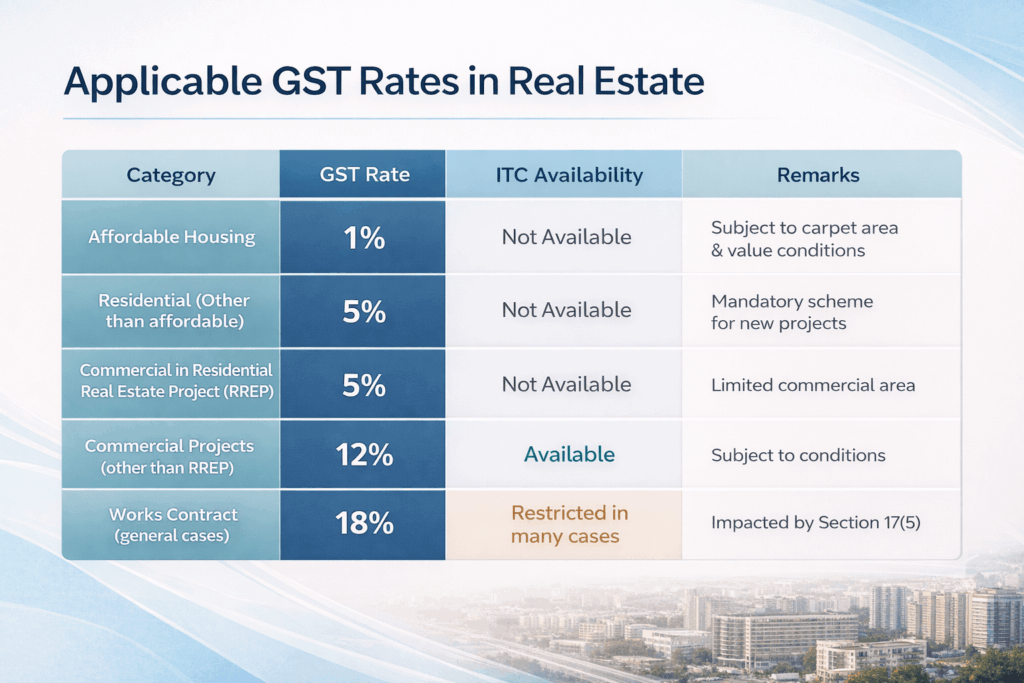

II. The 2019 Structural Overhaul – Policy Shift from ITC to Concessional Rates

Until 31 March 2019, residential projects were generally taxed at 12% with full input tax credit.

Through Notification No. 03/2019-Central Tax (Rate) dated 29 March 2019, the Government introduced a new scheme:

-

1% for affordable residential apartments (without ITC)

-

5% for other residential apartments (without ITC)

The Government also brought commercial apartments within a Residential Real Estate Project (RREP) under the 5% rate without ITC, subject to prescribed thresholds. Policymakers presented this shift as a measure to simplify taxation in the sector. However, commercially, it altered project costing in a fundamental way.

Under the earlier regime, embedded taxes on inputs such as cement (28%), steel (18%), and contractor services could be offset. Post-2019, such taxes became a cost component.

This shift also introduced:

-

80% procurement requirement from registered suppliers

-

Reverse charge mechanism (RCM) on shortfall procurement

-

RCM on cement purchases from unregistered persons

The policy reduced headline tax rates but increased compliance sensitivity and working capital pressures.

III. Input Tax Credit – The Epicentre of Litigation

1. Section 17(5) – Blocked Credits

Section 17(5)(c) and (d) of the CGST Act block ITC in respect of:

-

Works contract services for construction of immovable property (other than plant and machinery), except where used for further supply of works contract service.

-

Goods or services used for construction of immovable property on own account.

The phrase “on own account” has generated interpretational debate.

As of late 2024/2025, the Supreme Court of India delivered a landmark judgment in Chief Commissioner of CGST v. M/s Safari Retreats Pvt. Ltd. The Verdict: The Court upheld the “Functionality Test.” It ruled that if a building (like a mall or warehouse) is so uniquely designed that it serves the specific purpose of providing a service (renting/leasing), it can be treated as a “plant” under the exception to Section 17(5)(d). This means ITC is potentially available for commercial constructions intended for leasing, provided the taxpayer can prove the building functions as a “plant.”

2. Rule 42 & 43 – Proportionate Reversal and Unsold Inventory

Real estate projects often contain both taxable and non-taxable elements. Residential apartments (under new regime) do not permit ITC, whereas certain commercial components may.

Rule 42 and Rule 43 mandate proportionate reversal of common credits attributable to exempt supplies.

Additionally, Notification No. 03/2019 introduces a specific reversal mechanism for unsold units at the time of completion certificate.

This often results in significant ITC reversal at the end of the project lifecycle — a stage where liquidity may already be constrained.

Departmental audits frequently focus on:

-

reversal was done correctly.

-

area ratio was computed accurately.

-

turnover-based reversal was applied correctly.

IV. Joint Development Agreements (JDAs) – Taxability and Valuation Complexity

Joint development models are central to Indian real estate.

Typically:

-

Landowner transfers development rights.

-

Developer constructs.

-

Consideration is partly in constructed area.

1. Taxability of Development Rights

Notification No. 04/2019-Central Tax (Rate) provides exemption for transfer of development rights to the extent attributable to residential apartments remaining unsold at completion.

However, the valuation mechanism remains contentious.

In Pioneer Urban Land and Infrastructure Ltd. (AAR Haryana, 2019), the authority held that GST is payable on construction services provided to landowners, valued at the open market value of similar apartments.

Similarly, in Shree Dipesh Anilkumar Naik (AAR Gujarat, 2020), the authority examined valuation principles in development right transactions and adopted a strict interpretation of Rule 27.

While AAR rulings bind only applicants, they reflect the department’s valuation approach.

2. Time of Supply Issues

For construction services provided to landowners, liability typically arises at the time of completion or first occupation, as per notification framework.

However, structuring errors in agreements may inadvertently accelerate tax exposure.

Clear drafting becomes critical.

V. Ancillary Charges – Composite Supply or Independent Supply?

Developers frequently recover:

-

Preferential location charges (PLC)

-

Floor rise charges

-

Club membership

-

Car parking

-

Infrastructure development charges

In several advance rulings, authorities have held that when such charges are separately identifiable and optional, they may not automatically qualify as part of a composite supply.

For instance, in M/s. Bengal Peerless Housing Development Company Ltd. (AAR West Bengal, 2019), the authority analysed recoveries such as car parking and concluded that taxability must be independently examined. It is worth noting that while the AAR initially held that Preferential Location Charges (PLC) were a separate supply, the Appellate Authority for Advance Ruling (AAAR) and subsequent industry practice often view PLC as naturally bundled with construction. If the main construction service is exempt (post-completion), the PLC usually follows suit. PLC is taxed at the same rate, if it’s taxable (under-construction),

VI. Long-Term Lease of Land – Taxable or Exempt?

Long-term lease of land for residential projects has been subject to conditional exemptions.

However, lease premium structures for commercial developments have faced scrutiny.

In Greater Noida Industrial Development Authority (AAR Uttar Pradesh, 2018), the authority examined taxability of lease premium charged by statutory authorities.

The distinction between upfront premium and periodic lease rentals continues to invite interpretational challenges.

VII. Anti-Profiteering – The Continuing Exposure

Though the National Anti-Profiteering Authority (NAA) has been restructured, the statutory obligation under Section 171 continues.

Transitional projects remain vulnerable where documentation of cost adjustments is inadequate.

Since December 1, 2022, the Competition Commission of India (CCI) has officially taken over the functions of the National Anti-Profiteering Authority (NAA). While the article implies this, explicitly naming the CCI adds to its professional authority.

VIII. The 80% Procurement Rule – Compliance Sensitivity

Under the new scheme:

-

At least 80% of inputs and input services must be procured from registered suppliers.

-

Shortfall attracts RCM.

-

Cement from unregistered suppliers attracts RCM regardless of threshold.

This provision has significantly increased vendor compliance monitoring.

Failure to compute annual shortfall accurately may result in demand with interest.

IX. Judicial Trajectory – Where Are Courts Leaning?

High Courts have shown willingness to interpret GST in a manner consistent with value-added taxation principles.

Safari Retreats is an example of constitutional scrutiny.

However, in matters involving valuation and exemption notifications, courts have largely upheld strict statutory interpretation.

Real estate disputes are increasingly shifting from rate ambiguity to constitutional and structural questions around ITC denial and valuation methodology.

X. Key Risk Areas for Developers

From a practical perspective, the highest exposure arises in:

-

Incorrect ITC reversal on project completion.

-

Aggressive valuation in JDAs.

-

Misclassification of ancillary charges.

-

Non-compliance with 80% rule.

-

Inadequate documentation during rate transition.

-

Improper treatment of cancellation refunds.

Most demands today arise from audit scrutiny rather than rate misapplication.

Conclusion – Stabilised in Form, Litigative in Substance

The GST regime for real estate has achieved rate stability since 2019. Yet, litigation persists because:

-

ITC restrictions challenge value-added principles.

-

Development right transactions involve complex valuation.

-

Composite supply doctrine is narrowly interpreted.

-

Anti-profiteering remains an enforcement tool.

For developers and finance heads, the focus must shift from rate application to structural compliance, documentation discipline, and periodic GST health reviews.

In a sector where projects span multiple financial years and tax positions crystallise at completion stage, proactive legal analysis is indispensable.

The real estate industry under GST is no longer uncertain — but it remains intensely scrutinised.